Article

Strategies for Building a Laddered Retirement Portfolio

If the goal of saving for retirement is to provide financial

security, then a key objective of retirement portfolio management

should be generating a stable stream of income while preserving

investment principal. Bond laddering is a strategy that may address

both aspects of that key objective.

What Is Laddering?

A bond ladder is a portfolio of bonds with maturity dates that

are evenly staggered so that a constant proportion of the bonds can

be redeemed at par value each year. By holding bonds to maturity

rather than trying to buy and sell them in the secondary market,

investors may minimize the potential for losses caused by interest

rate volatility and market inefficiency. These losses and

transaction costs can be considerable.

Generally speaking, there are two broad types of bond ladders.

One can be implemented more or less perpetually for trusts,

endowments, and other applications with extended planning horizons.

Another form of bond ladder can be implemented for individuals

whose personal financial plans might have a definite end-point in

mind. Both types of ladders can potentially play a role in reducing

some bond market risks.

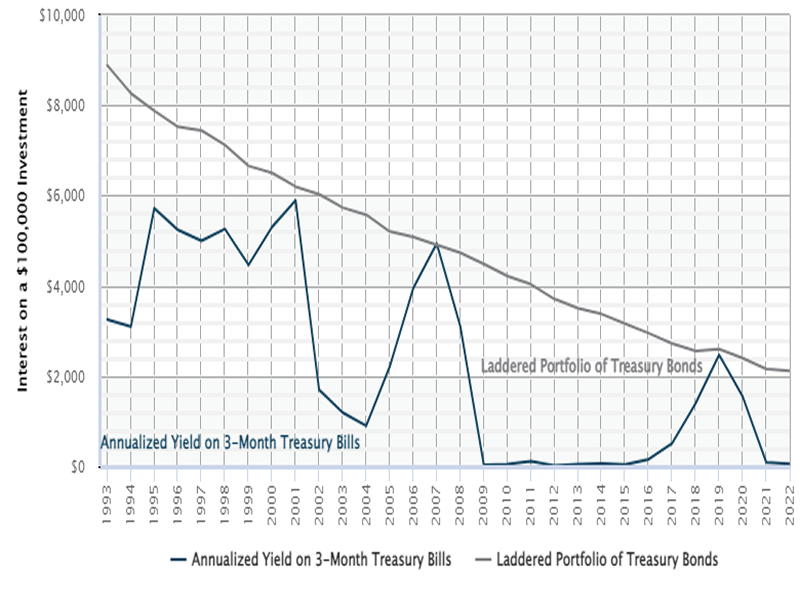

Perpetual Bond Laddering

This bond laddering strategy is most useful for an investor who

plans to conserve investment capital indefinitely and whose need

for cash flow is predicable. A typical ladder might be constructed

from Treasury bonds, with one-tenth of the portfolio being redeemed

and reinvested each year. As the following chart shows, such a

structure would have been significantly more productive and less

volatile over the past four decades than a strategy of simply

buying and rolling over short-term notes, such as three-month

Treasury bills. Keep in mind, however, that the long bond ladder is

significantly less liquid than a short bill portfolio. Virtually

all of the assets in the short portfolio can be liquidated at face

value within three months. In contrast, only 10% of the long

portfolio can be liquidated at face value in any given year; the

remaining 90% might be exposed to considerable market and interest

rate risk if it were sold in the secondary market rather than held

to maturity.

| Comparing the Continuing Cash Yields of

Two $100,000 Investments |

|

Source: ChartSource®, SS&C Retirement

Solutions, LLC. For the period from January 1, 1993, through

December 31, 2022. Assumes a ladder of 10 years created in 1993,

where all bonds mature on December 31 of the given year, principal

amounts were rolled over into new 10-year bonds with then-current

market yields, and that interest payments were not reinvested.

Yields are based on yield data published by the Federal Reserve and

are imputed for maturities that the Federal Reserve does not report

(generally, 4-, 6-, 8-, and 9-year bonds). Using a bond ladder

strategy does not guarantee superior results. Index performance

does not reflect the effects of investing costs and taxes. Actual

results would vary from benchmarks and would likely have been

lower. Past performance is not a guarantee of future results.

© 2023 SS&C. Reproduction in whole or in part prohibited,

except by permission. All rights reserved. Not responsible for any

errors or omissions.

Laddering With a Fixed Term in Mind

Another type of bond ladder is one built to provide a steady

cash flow for a predetermined number of years. This can be done

with a zero-coupon bond, a type of bond that pays all of its

interest in one lump sum at maturity. Generally speaking, the

further in the future that one expects to receive the redemption

value, the less one needs to spend today for the bond.

Here is how the principal of a fixed-term bond ladder can be

applied to the needs of a retirement investor. In this hypothetical

example, the retirement portfolio is worth $250,000 at retirement

and the presumed withdrawal rate is 4% of assets per year, or

$10,000. Based on the interest rates that prevailed at the end of

2019, an investor could buy a series of 20 zero-coupon Treasury

bonds, one of which would become redeemable in each of the next 20

years. The total discounted cost of those 20 bonds would be

approximately $156,000. The balance of the original $250,000 could

be allocated to equities for growth potential, creating a portfolio

that still holds more than 30% equities. The core income of $10,000

would be stable, and the value of the equity portfolio should be

available to help augment income as needed to compensate for

inflation or provide extra latitude for spending. Equity value

could also be available to extend the term of the plan if needed.

Planning horizons of greater than 20 years can also be addressed at

the outset, albeit at somewhat greater cost. Note also that bonds

in the ladder will have value during the course of the plan, even

though their value may be subject to fluctuations caused by

interest rate volatility.

| Investment Needed to Create

$10,000 Per Year |

| Term |

Immediate total investment needed |

| 20 years |

$156,000 |

| 25 years |

$183,000 |

| 30 years |

$206,000 |

| Source: SS&C Technologies, Inc. Indicated costs

assume the initial amounts are invested in zero-coupon U.S.

Treasury bonds maturing on the anniversary dates of the investment

and yielding the market rate for that maturity that prevailed on

December 31, 2019. Estimated investment needs for similar ladders

created on other dates will vary -- increasing as prevailing market

yields fall and decreasing as prevailing yields rise. This

hypothetical example does not account for potential custody

expenses, transaction costs, or tax liabilities, if any. The value

of Treasury bonds can be assured only when they are held to

maturity and redeemed by the U.S. government. Until redemption

time, the market value of Treasury securities varies as prevailing

interest rates rise and fall. Past performance is not a guarantee

of future results. |

Work With a Professional

An investment portfolio that has some of its assets allocated to

bonds may produce stronger cash flow with less volatility than a

portfolio allocated solely to equity investments such as common

stock shares. As such, a bond ladder offers investors a formula for

allocating their fixed-income holdings to potentially reduce the

unique risks of bond holdings and to achieve the results they seek

from their bond investments. Your financial professional can help

you determine whether bond laddering is an efficient solution for

your needs.

The Language of Bonds

- Par value is the face value of the bond (i.e.,

the value the bond was assigned when the issuer created it).

- Market value is the price for which a bond can

be bought or sold at any given time after it is issued and before

it is redeemed in the process known as secondary market trading.

The prices of bonds in the secondary market depend on the overall

level of interest rates. Prices of existing bonds rise when the

general level of interest rates falls, and prices fall when the

general level of interest rates rises. Individual bond prices can

rise relative to their peers in the secondary market if the

creditworthiness of the borrower improves, or they can lose ground

relatively if the creditworthiness of the borrower

deteriorates.

- Redemption value is the amount of money that

the issuer will return to the investor on the specified maturity

date. Redemption value is generally not affected by changes in the

secondary market price.

- Maturity date is the date set for repayment of

the bond's principal; it is normally established at the time the

bond is issued. A conventional bond is issued for

a fixed period. A callable bond can be redeemed at

the initiative of the issuer whenever the call conditions specified

in the bond are met. A putable bond can be

redeemed at the initiative of the investor whenever the specified

put conditions are met. A convertible bond is one

that can be exchanged for common stock at specified times.

- Coupon value is the cash amount of the

interest payment made to the investor each year. In most cases, the

coupon value never changes throughout the life of the bond,

regardless of any changes in secondary market value of the

bond.

- Coupon yield is the value of the interest

payment given to the investor each year expressed as a percentage

of the original par value of the bond. This figure does not change

during the life of the bond.

- Current yield is the value of a bond's

interest payment expressed as a percentage of its current trading

price in the secondary market. Current yield is actually the

primary basis for defining a bond's trading price in the secondary

market because current yields on existing bonds need to maintain

their relationships with market averages. To keep yields

synchronized with the market, trading prices are adjusted. Lowering

a bond's price has the effect of increasing its current yield

because the coupon payment would be divided into a smaller market

value. Increasing a bond's price has the effect of lowering the

current yield because the coupon payment would be divided into a

larger market value.